Date: May 29, 2026

Author: Fintech Cafe Editorial Team

The Million-Dollar Tax Bill That Never Happened

In late 2025, a technology entrepreneur sat across from her private banker with a familiar dilemma.

Her wealth had grown dramatically over the previous decade. Most of it sat in a concentrated equity position worth nearly $80 million. The shares had appreciated significantly, creating a substantial unrealized gain.

At the same time, she wanted to purchase a waterfront property, invest in a private equity opportunity, and establish a family trust structure for the next generation.

Selling shares would generate liquidity—but also trigger a sizable capital gains tax bill.

Instead, her advisor proposed a different solution.

“What if you never had to sell?”

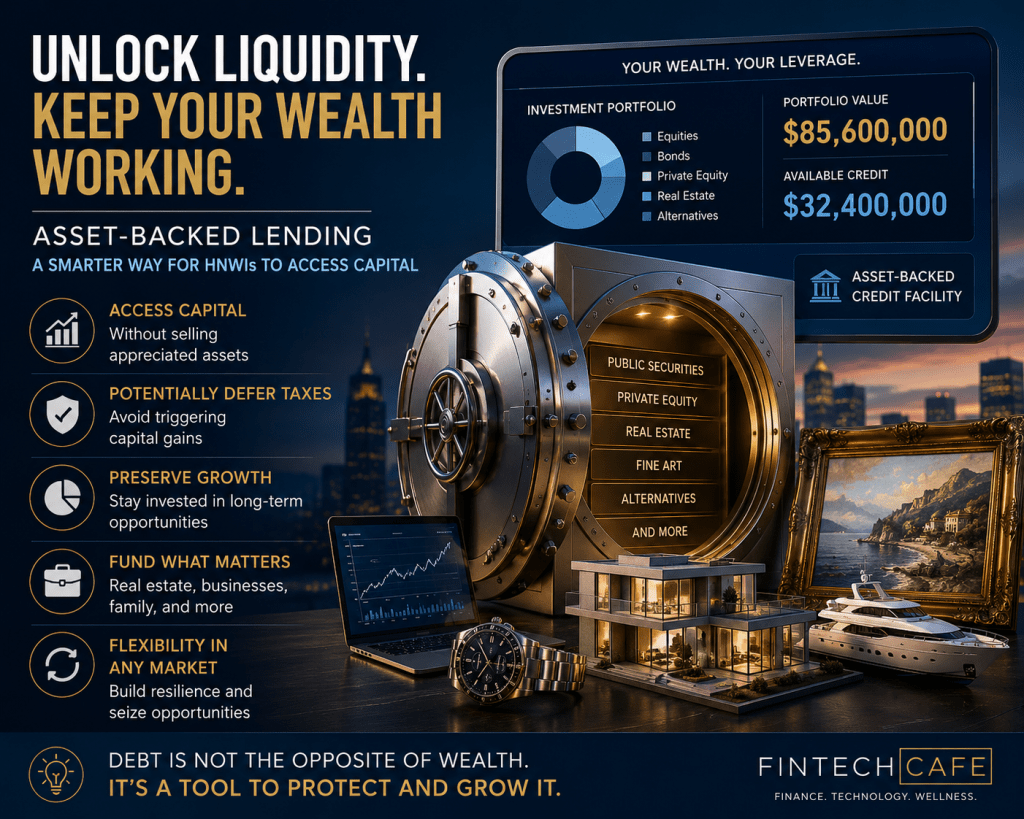

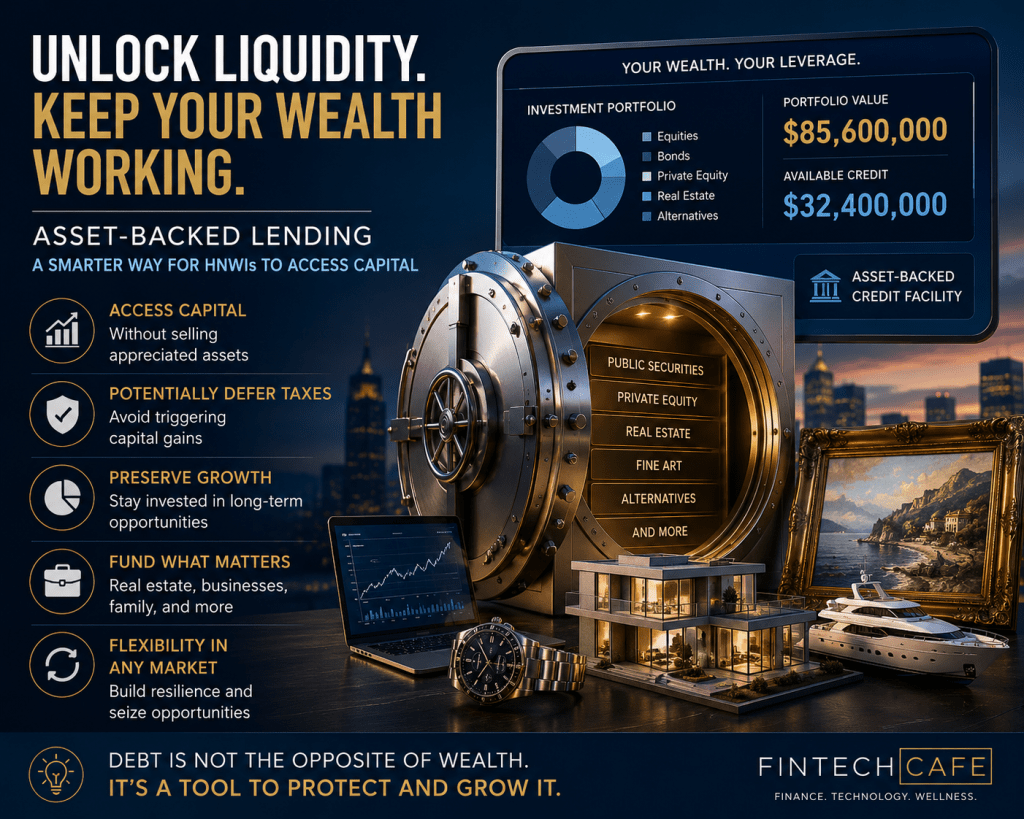

Within weeks, the entrepreneur secured a multi-million-dollar credit facility backed by her investment portfolio. The transaction unlocked liquidity, preserved ownership of appreciating assets, deferred taxes, and provided flexibility to pursue multiple opportunities simultaneously.

This is the power of asset-backed lending—a strategy increasingly becoming a cornerstone of sophisticated wealth management.

The Rise of Lending Against Wealth

For decades, wealthy families have understood a simple principle:

The most tax-efficient asset sale is often the one that never happens.

Asset-backed lending (ABL) allows investors to borrow against existing assets rather than liquidating them. These assets may include:

- Public securities portfolios

- Private company shares

- Commercial real estate

- Fine art collections

- Aircraft and yachts

- Insurance policies

- Alternative investments

- Private equity and hedge fund interests

The concept is straightforward: assets serve as collateral for a loan, enabling owners to access liquidity while maintaining ownership and potential future appreciation.

Yet the implications are profound.

As wealth creation increasingly concentrates in illiquid assets—private businesses, venture investments, and concentrated stock positions—the demand for flexible liquidity solutions has accelerated.

Private banks and family offices now view lending not merely as a banking product but as a strategic wealth management tool.

Why HNWIs Are Borrowing More Than Ever

Three structural trends are driving adoption.

1. The Tax Efficiency Imperative

Consider an investor with a $20 million stock position purchased for $2 million.

Selling $5 million worth of shares may generate substantial tax liabilities depending on jurisdiction and holding structure.

Borrowing against those same shares can provide immediate liquidity without crystallizing gains.

While interest costs must be considered, many investors view the trade-off favorably when compared with the immediate tax impact of liquidation.

2. The Opportunity Cost of Selling

Markets have repeatedly rewarded long-term ownership.

A family that sells strategic holdings to fund lifestyle needs risks missing future appreciation.

Asset-backed lending allows investors to separate liquidity decisions from investment decisions.

Instead of asking:

“Should I sell?”

The question becomes:

“How should I finance this opportunity?”

This subtle shift often creates significant long-term value.

3. Wealth Is Becoming Less Liquid

According to multiple global wealth studies, an increasing share of HNWI wealth resides in private markets.

Founders, executives, and investors frequently hold substantial wealth in:

- Private businesses

- Venture capital positions

- Restricted stock

- Alternative investments

These assets may be valuable on paper yet difficult to monetize quickly.

Asset-backed lending bridges this gap.

The Modern Private Banking Playbook

Today’s leading private banks increasingly position lending capabilities alongside investment advisory services.

The rationale is simple.

Clients rarely experience wealth in neat categories such as investments, borrowing, philanthropy, and estate planning.

Instead, their financial lives are interconnected.

A securities-backed line of credit may fund:

- Real estate acquisitions

- Business expansion

- Tax obligations

- Philanthropic commitments

- Lifestyle purchases

- Bridge financing ahead of a liquidity event

The best advisors therefore view lending as an integrated component of balance-sheet management rather than a standalone credit product.

Beyond Securities: The Expansion of Collateral

One of the most significant developments in recent years has been the broadening of acceptable collateral.

Historically, liquid securities dominated lending programs.

Today, lenders are increasingly willing to structure facilities against:

Private Company Equity

Founders often hold significant wealth before a liquidity event.

Specialized lenders now provide financing against private shares under carefully structured arrangements.

Luxury Assets

Fine art, collectibles, aircraft, and yachts are becoming more financeable.

Dedicated lenders have emerged to evaluate and monetize these traditionally illiquid holdings.

Alternative Investments

Private equity and hedge fund interests are increasingly accepted as collateral, particularly among institutional-grade borrowers.

This evolution reflects a broader trend:

Banks are adapting to how modern wealth is actually held.

The Risks Investors Must Understand

Asset-backed lending is powerful, but it is not risk-free.

The most important risk is collateral volatility.

If market values decline significantly, lenders may require:

- Additional collateral

- Partial repayment

- Asset liquidation

This dynamic became highly visible during periods of market stress when leveraged investors faced margin calls.

For concentrated positions, the risk can be amplified.

A single stock decline may trigger collateral concerns far more quickly than a diversified portfolio.

Investors must also consider:

- Interest rate exposure

- Liquidity requirements

- Loan-to-value thresholds

- Concentration limits

- Regulatory and tax implications

The objective should never be maximizing leverage.

The objective should be maximizing flexibility while preserving resilience.

The Family Office Perspective

Many family offices increasingly view debt as a strategic asset rather than a liability.

This mindset differs from traditional retail finance.

For affluent families, borrowing is often less about necessity and more about optimization.

Debt can preserve investment exposure, smooth liquidity management, and create optionality during periods of market uncertainty.

When structured prudently, asset-backed lending allows families to keep capital invested while addressing short-term cash requirements.

In this sense, lending becomes an enabler of long-term wealth preservation.

The Future: Digital Lending Meets Private Wealth

Technology is transforming the asset-backed lending landscape.

Artificial intelligence, real-time portfolio analytics, and automated collateral monitoring are reducing underwriting friction.

Fintech platforms are increasingly capable of:

- Continuous collateral valuation

- Faster approval processes

- Digital loan origination

- Predictive risk monitoring

- Integrated wealth dashboards

As private banking embraces digital transformation, lending is likely to become more personalized, more responsive, and more deeply integrated into broader wealth management ecosystems.

The next generation of affluent clients expects the same speed and convenience from liquidity solutions that they receive from investment platforms.

The institutions that can deliver both will have a significant competitive advantage.

Key Takeaway

Asset-backed lending is no longer a niche strategy reserved for the ultra-wealthy.

It has become a fundamental liquidity management tool for high-net-worth investors seeking to preserve ownership, defer taxes, and maintain investment exposure while accessing capital.

Used responsibly, it enables investors to unlock the value of their assets without surrendering them.

For many wealthy families, that distinction may prove one of the most important advantages in modern wealth management.

Sources

- Capgemini World Wealth Report (latest editions)

- McKinsey & Company research on private wealth and family offices

- UBS Global Family Office Reports

- EY Global Wealth Management studies

- Bain & Company wealth management insights

- Institutional Investor and Private Banker International industry coverage

Leave a comment