𝑏𝑦:𝐹𝑖𝑛𝑡𝑒𝑐ℎ𝐶𝑎𝑓𝑒 𝐸𝑑𝑖𝑡𝑜𝑟𝑖𝑎𝑙

𝐽𝑢𝑛𝑒 26,2026

Most private banks are building better portals for a problem that stopped being about portals three years ago.

The next generation of UHNW clients doesn’t need a sleeker dashboard. They need advisors who can think across an entire family enterprise — investments, credit, liquidity, governance, tax, real estate, succession — simultaneously, in real time, at institutional quality.

That is a fundamentally different service model than what most institutions currently deliver. The gap between those two things is widening faster than most firms want to admit.

The Inheritance Problem

When wealth transfers to the next generation, it rarely arrives as a simple portfolio.

ⵊᴛ ᴀʀʀɪᴠᴇs ᴀs ᴀ ꜰᴀᴍɪʟʏ ᴇɴᴛᴇʀᴘʀɪsᴇ.

That enterprise may include concentrated public positions, private equity stakes, operating businesses, real estate across multiple jurisdictions, outstanding credit facilities, capital call obligations, trust structures, philanthropic commitments, embedded tax complexity — and all of it managed across multiple providers who do not talk to each other.

The traditional UHNW service model was not built for this. It was built for a simpler world: relationship management, investment access, lending, estate coordination. Fragmented by design. Siloed by institution.

That model worked for the generation that built the wealth, because fragmentation was the norm and the advisor’s primary job was investment alpha plus relationship continuity.

The next generation grew up with real-time data, cross-platform transparency, and the expectation that complexity should be made manageable — not explained away. They are not tolerating fragmentation. They are replacing the advisors who deliver it.

𝗔𝗜 𝗜𝘀 𝗡𝗼𝘁 𝘁𝗵𝗲 𝗔𝗻𝘀𝘄𝗲𝗿. 𝗜𝘁’𝘀 𝘁𝗵𝗲 𝗔𝗰𝗰𝗲𝗹𝗲𝗿𝗮𝗻𝘁.

The industry conversation about AI in wealth management has largely missed the point.

The most valuable near-term application of AI in the UHNW context is not a robo-CIO making autonomous allocation decisions. That use case is both premature and mostly irrelevant to families whose real complexity sits outside the liquid portfolio.

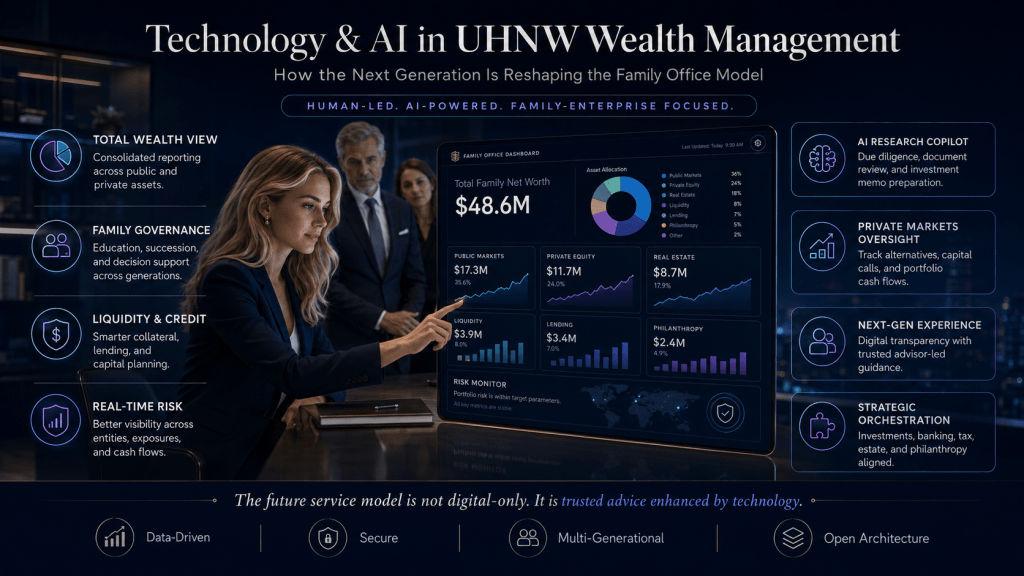

The real opportunity is at the operating layer — the work that currently consumes advisor time without producing proportional client value:

- Investment research synthesis and manager due diligence review

- Capital call and distribution tracking across private market commitments

- Risk concentration monitoring across custodians and entities

- Tax-lot and collateral analysis in support of credit decisions

- Liquidity forecasting across the family balance sheet

- Consolidated reporting across asset classes, jurisdictions, and structures

- Meeting preparation, documentation, and follow-up

AI accelerates all of this. That matters because the advisor’s highest-value contribution was never information delivery — it was judgment. The ability to translate complexity into clarity, connect decisions to long-term family outcomes, and earn trust in high-stakes moments.

Every hour an advisor spends manually reconciling data across six custodians is an hour not spent on the conversation that retains the next generation.

AI returns those hours. What advisors do with them will determine who wins this client segment over the next decade.

Credit Is the Most Undervalued Strategic Tool in the Family Office

This is where the service model has most consistently underdelivered — and where next-generation expectations will force the sharpest change.

In most private banking relationships, credit is treated as a transaction. A securities-backed line. A real estate loan. A capital-call bridge. Priced, documented, deployed, forgotten.

Tʜᴀᴛ ɪs ɴᴏᴛ ᴡʜᴀᴛ ᴄʀᴇᴅɪᴛ ɪs ꜰᴏʀ.

In a sophisticated family enterprise, credit is balance-sheet architecture. The right structure can provide liquidity without forcing asset sales at the wrong moment, bridge timing gaps between PE commitments and distributions, fund private market allocations without disrupting the liquid portfolio, support estate transfer strategies with tax-efficient precision, and create strategic flexibility during market dislocations — all without triggering unnecessary realization events.

The next generation will not ask “what rate can you offer?” They will ask what the credit facility is actually doing inside their capital structure. Whether the collateral pool is resilient enough to survive a 30% drawdown. How the pledge interacts with pending capital calls. Who inside the family has the authority to borrow, repledge, or repay. What the tax and estate implications are before the line is activated.

Advisors who can answer those questions become structural partners in the family enterprise.

Advisors who cannot will be treated as commodity lenders — and priced accordingly.

Governance Is Not Soft. It Is the Load-Bearing Wall.

The section most firms skip because it doesn’t fit neatly into a product conversation.

As wealth transfers across generations, the most common failure mode is not investment underperformance. It is decision-making breakdown — unclear authority over borrowing, inconsistent distribution policies, unresolved tension between family members with different views on risk, liquidity, and legacy.

Technology cannot fix this. A better portal will not define who has the authority to pledge family assets. AI cannot mediate a disagreement between siblings over whether to sell the operating business.

The next-generation service model requires governance infrastructure: clear decision rights, defined borrowing authority, financial education frameworks built before inheritance happens, succession plans that account for all stakeholders, and communication structures that prevent tension from becoming crisis.

This is where the advisor’s value is most difficult to replicate — and most difficult to lose. Technology absorbs complexity. Human judgment navigates people.

The advisors who are competent in both will define what UHNW wealth management looks like in 2035.

Tʜᴇ Tʀᴀᴘ: Dɪɢɪᴛɪᴢᴀᴛɪᴏɴ Dɪsɢᴜɪsᴇᴅ ᴀs Tʀᴀɴsꜰᴏʀᴍᴀᴛɪᴏɴ

Most institutions will respond to this shift by investing in technology — richer dashboards, AI-assisted reporting, slicker mobile experiences, consolidated data aggregation.

Some of that investment will help. None of it is sufficient on its own.

A dashboard without interpretation is an expensive spreadsheet. Data without context is noise. AI without governance is a liability. Technology without trust will not retain a UHNW family across a generational transition.

Transformation is not a product launch. It is a service model redesign — one where technology absorbs operational complexity so that the human advisor can operate at a genuinely higher level: orchestrating across investments, credit, liquidity, tax, governance, and family dynamics at the same time, in service of a single coherent family strategy.

That requires advisors who are technically literate, emotionally intelligent, and willing to have conversations that extend well beyond portfolio performance.

Most institutions say they want to build for this. Fewer actually are.

The Advisor Becomes an Orchestrator

The UHNW advisor of the next decade is not primarily an investment guide.

The highest-value advisor will coordinate across CIOs, credit specialists, estate attorneys, tax advisors, trustees, family office executives, and next-generation family members — not to have every answer personally, but to ask better questions, connect the right expertise at the right moment, and help families make consequential decisions with clarity rather than conflict.

The value will not come from information access. Every client already has that.

It will come from judgment, synthesis, and the kind of trust that survives a market crisis, a family dispute, or a generational transition.

The families that find advisors capable of this will build multigenerational enterprises.

The ones that don’t will fragment — slowly, then suddenly.

The future of UHNW wealth management is not digital-only.

It is trusted advice, enhanced by technology, organized around the family as an enterprise.

The advisors who internalize that shift will become more valuable.

The ones who are still waiting for their institution to explain it to them are already behind.

Leave a comment